Inflation is back (see last week’s BBTW), and President Donald Trump says he’s got nothing to do with it. Three percent inflation in January had the Fed set aside plans to make further rate cuts this year, since much of the price hikes were due to consumers and businesses anticipating Trump’s planned tariffs. In a conversation with Fox personality Sean Hannity, Trump, seated at the right hand of First Buddy Elon Musk, spontaneously told Hannity, “Inflation is back.”

“I’m only here for two and a half weeks,” Trump said (though it’s actually been a month since inauguration). “I had nothing to do with it,” Trump continued. “They spent money like nobody has ever spent.” Yeah…but ever since Trump took a lead in the polls in September, consumer expectations that he’d send prices rising have been a self-fulfilling prophecy, according to Moody’s chief economist, Mark Zandy. “Anticipation of the president’s economic policies, as they have resulted in higher inflation expectations,” are probably one driver of the price increases. Trump campaigned on bringing prices down on “day one” of his second term after pandemic-fueled price hikes pushed inflation to 9%. Reality bit in December when Trump started to back down, telling Time Magazine “It’s hard to bring things down once they’re up. You know, it’s very hard.”

That’s no excuse for the Fed. Minutes of the Fed’s last meeting reveal serious concern about whether Trump’s policies will help the economy. Fed officials said Trump’s tariffs and mass deportations—along with strong consumer spending—could push inflation higher this year. Economists agree: Only 10% of 47 economists on a panel compiled by consulting firm WoltersKluwel expect a rate cut at the Fed’s March meeting, and 80% say tariffs will provide “a significant boost” to U.S. inflation. In the minutes, Fed governors said they expect that firms will pass their own higher costs from tariffs onto consumers. Greg Daco, chief economist at consultants EY, said he expects two rate cuts this year: June and December. He warns it all depends on how much the Trump economic agenda boosts inflation. “The risk is tilted toward less easing if the administration’s policy mix fuels higher inflation and inflation expectations.”

The Fed’s pause means that borrowing costs for consumers, including mortgages, auto loans, and credit cards won’t be dropping anytime soon.

The Usual Suspects

- Uber’s DoorDash feud: Uber is suing its biggest competitor, DoorDash, saying it threatened hiking its commission charge for restaurants that also continue to use Uber Eats. The apps already charge restaurants a hefty commission, running as high as 30% of the menu price. DoorDash has a stranglehold on the business, holding 63% of the U.S. delivery market in 2024, followed by Uber with 25% and Grubhub with 6%. “DoorDash’s coercive tactics reduce restaurant-customer and consumer choice, resulting in higher prices, lower-quality service, and decreased innovation,” Uber said in the complaint. “Uber’s case has no merit,” countered DoorDash. “Their claims are unfounded and based on their inability to offer merchants, consumers, or couriers a quality alternative.”

- Apple’s big, cheap beautiful new iPhone: Apple’s gone solo, with the introduction of its new, lower-priced iPhone 16e this week, selling for $599. The phone is built on the first cellular chip Apple developed itself, the C1, in a push for tech autonomy (and a hope to wean itself off of chips from cell-phone rival Qualcomm). Analysts see the phone as a test of Apple’s new technology, likely to roll out this fall with the iPhone17. Apple really, really wants to go splitsville with Qualcomm. In 2017, it sued Qualcomm over the chip maker’s licensing practices. Not only does Apple have to pay for every wireless modem chip it buys, but it has to pay another $5 to $6 per chip for Qualcomm’s wireless licenses. A homemade chip would save Apple billions a year.

- FTX makes good? Well kinda, sorta, not really. Sam Bankman-Fried’s fraud-riddled crypto exchange FTX Digital markets will begin repaying $1.2 billion to creditors. Unfortunately for those caught in the FTX machinations, they’ll only get back about $20,000 for each lost Bitcoin, since that’s the price it was trading for when the exchange collapsed. The price is now hovering just under $100,000, and creditors are upset they’ve lost the chance to see their holdings rise. On the other hand, the currency’s five-fold appreciation means the administrators of the failed exchange actually have some cash to pay back the creditors. At current prices, FTX owes about $11.2 billion and has between $14.5 and $16.3 billion to pay back its creditors.

- Media matters: Donald Trump’s lawsuit against CBS and its 60 Minutes program for allegedly editing an interview with Kamala Harris to mislead voters is proving a major thorn in the side of parent Paramount while it seeks to avoid antitrust scrutiny over its planned sale to Skydance Media. Trump alleged Harris’ words were changed, even as multiple examinations of the full tapes show no evidence of a switch. Still, he’s threatening to bankrupt Paramount with a $20 billion lawsuit. Paramount’s board is in a dilemma—do they pay off Trump to let the merger go ahead, or do they fight? Either way, shareholders may sue them for giving in or bailing out. However, a negotiated end is possible, as Skydance’s owner is the son of Trump tech-buddy, inauguration front-row seatholder, and Oracle-founder Larry Ellison. Remember that famous CBS sitcom All in the Family?

- Southwest jobs go south: Discount carrier Southwest Airlines said it is shaving 1,750 jobs from its executive ranks (about 15% of its corporate workforce) under pressure from activist investors to cut costs. CEO Bob Jordan said that executive ranks have been growing faster than revenue, and Southwest is also facing cash pressure from new union contracts. It’s also been hit by delays in delivering new planes at Boeing, which is keeping Southwest from adding flights to heavily travelled routes.

- Kentucky what? Says KFC: Louisville is saying good-bye to Col. Sanders, after KFC parent Yum Brands decided to move the headquarters of the fried chicken joint formerly known as Kentucky Fried Chicken to Planoi, Texas. Yum Brands and charitable organization the KFC Foundation will keep their corporate offices in Louisville, while Yum brand Pizza Hut is already based in Plano. “This company’s name starts with Kentucky, and it has marketed our state’s heritage and culture in the sale of its product,” said disappointed Kentucky governor Andy Beshear. When “Colonel” Harlan Sanders, the chain’s founder, died in 1980, he lay in state at the Kentucky State Capitol.

- Microsoft’s Cat? Every college student learned about Schrodiner’s cat, which by the rules of quantum mechanics could be both alive and dead at the same time. Microsoft says it created a new state of matter to build a quantum computer that would make easy work of the world’s most complex calculations, outsripping the ability of generative artificial intelligence and synthetic neural networks. Microsoft scientists say they’ve built a “topological qubit” based on this new phase of physical existence, which could be harnessed to solve mathematical, scientific, and technological problems. The science is complex, but the business case is clear. Microsoft could easily bypass Google now, which last year showed off an experimental quantum computer that the New York Times reported needed just five minutes to complete a calculation that most supercomputers could not finish in 10 septillion years.

What do you think of Big Business This Week? Tell us how you really feel in this survey!

Elon’s World

OpenAI’s board has officially rejected Elon Musk’s $97.4 billion to buy the AI company led by Musk’s new archenemy, Sam Altman. The bid is “not in the best interests” of OpenAI, the company wrote in a letter to Musk. Musk has been suing in federal court to block Altman’s plans to turn OpenAI from a non-profit to a for-profit company. Musk has said the conversion would be a betrayal of OpenAi’s mission, in which he had originally invested millions of dollars. OpenAI is also a competitor with Musk’s lagging xAI artificial intelligence company. Musk formally withdrew his offer on Wednesday, but as The Wall Street Journal reported, Musk attorney Marc Toberoff said the board should have considered his client’s offer in good faith because the for-profit conversion is a sham. “They’re just selling it to themselves at a fraction of what Musk has offered,” he said, accusing the board of a “classic self-dealing transaction.”

Remember when talk of love swirled around Musk and Girogia Meloni, the Italian prime minister? That seems to be very old news now, as a senior Italian government minister said Italy is developing its own web of low-orbit satellites to avoid having to depend on Musk’s Starlink satellite service. Musk was photographed in intimate conversation with Meloni after he presented her with the Atlantic Council Global Citizen Award, saying it was an honor to give the award to “someone who is even more beautiful on the inside than she is on the outside.”

Trump fired a warning shot across Musk’s bow this week, telling Fox News’ Sean Hannity that it would be “unfair” to the U.S. if Musk built a car factory in India to avoid that country’s high tariffs on imported cars. Car tariffs were a key point of discussion when Indian PM Narendra Modi visited Washington last week.

Get Big Business This Week in your inbox every week—and read it before everybody else! Sign up today.

The Short Stack

- Who wants AI, anyway? Not America’s corporate chieftans, The Wall Street Journal reports, citing attendees at its annual CIO summit. Some 61% of CIO’s said they’re experimenting with AI agents, while 21% said they’re not using them at all. Their top concern about AI: It’s unreliable. Meanwhile, the big AI vendors, like OpenAI, Microsoft and Sierra say if the buyers wait for AI to get it right, it will be too late. Hmmm.

- SoftBank’s soft quarter: Fresh off a joint announcement with Sam Altman and Donald Trump that he’d partner with U.S. companies to invest up to $500 billion in new AI infrastructure in the U.S., SoftBank CEO Masayoshi Son reported his company had a net loss of $2.42 billion in Q4, raising questions about its ability make those promised investments. Anyone competing with xAI gets a broadside from Elon Musk, who openly questioned the seriousness of the big AI bet, called Stargate, after he was not present at the announcement. SoftBank CFO Yoshimitsu Goto said the company has long experience in project finance and doesn’t need to rely solely on its own balance sheet for investment funds. “We hope Elon-san will find that out,” he said.

- The California fires bite back: The cost of those fires is about to hit. California’s state-sponsored insurer of last resort, the FAIR Plan, says it will collect $1 billion from private insurers in the state, triggering an automatic increase in private home insurance across California. Already, major insurers were pulling back from the state. The money is needed for FAIR to pay out its claims, said the state’s insurance commissioner Ricardo Lara. Half the cost of the assessment can be passed on to consumers. Insurers have to absorb the other half. That’s pushing up rates. State Farm last week asked Lara to let it raise rates by 22% to keep operating in California. Advocates are also hoping the debacle will encourage insurers and the states to require less risky home-building practices, particularly the rapid growth of housing in the so called Urban-Wildland Interface, and the replacement of aging high-tension lines that sparked the 2017–2018 wildfires.

- Murdoch’s latest media move: Rupert Murdoch’s Fox Corporation said it’s acquired Red Seat Ventures, the digital media company that has become a go-to partner for conservative old-media stars, including Megyn Kelly, Tucker Carlson and Piers Morgan, as they create their own online programming. Red Seat founders Chris and Kevin Balfe will operate autonomously inside Fox’s Tubi Media Group. The purchase price was not disclosed. The move represents a homecoming for Carlson, who was pushed out of Fox TV as his program aired increasingly bizarre conspiracy theories and Russian state propaganda. Also coming aboard as part of Red Seat: Dr. Phil, Nancy Grace and another disgraced Fox personality, Bill O’Reilly.

Trumplandia

- Bribe, baby, bribe! U.S. companies have long complained they’ve been sidelined in countries where payoffs to government officials are the way to get business done. That’s because under the 1977 Foreign Corrupt Practices Act, it is illegal for U.S. companies to pay bribes abroad. The law was put in place following revelations by a Senate committee of massive bribes paid by U.S. firms, including Northrop, Lockheed, United Brands, Gulf Oil, and Mobil in Saudi Arabia, Japan, Honduras, Korea, Italy, and the Netherlands. United Brands CEO Eli Black jumped to his death from Manhattan’s PanAm building in 1973 just before investigators discovered a bribe he’d paid to Honduras’s president to cut taxes on banana exports. Black’s son Leon runs Apollo Capital Management. In one notable case brought under the FCPA, a Goldman Sachs subsidiary pleaded guilty to a foreign bribery charge in the collapse of Malaysia’s 1MDB sovereign wealth fund, with the bank paying $2.9 billion in fines and penalties and a former Goldman banker sentenced to 10 years in prison. Now Trump wants to sideline the law. In one the scores of executive orders he’s signed since returning to the White House, Trump has ordered the Justice Department to pause criminal investigations under the law for 180 days. It’s not clear how that affects civil prosecutions, which are handled by the Securities and Exchange Commission, and can result in fines of many millions of dollars. The White House said in a fact sheet Monday that U.S. companies were harmed by “overenforcement” of the act, because it “prohibited [them] from engaging in practices common among international competitors, creating an uneven playing field.”

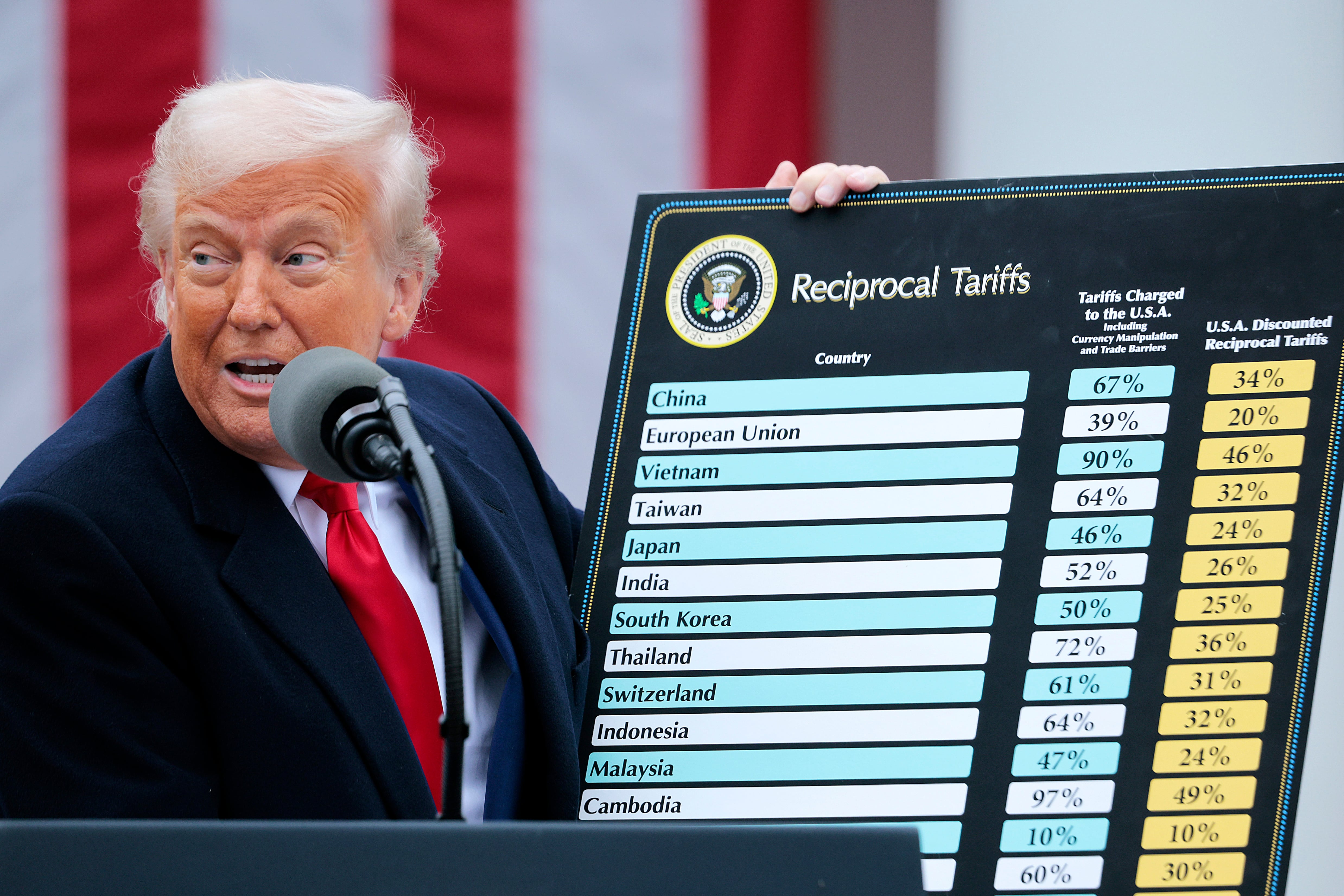

- The tariff mess: Trump’s proposed tariffs are starting to cause a world of hurt, even before they are enacted. Planned 25% tariffs on steel and aluminum imports, set to take effect on March 12, are likely to hit automakers hard, and it will take time for U.S. steel mills to ramp up, even as their plants have excess capacity of more than 30%, and imports count for only 26% of U.S. steel demand. But getting the right mix of steel at the right price is why imports are used in the first place. A proposed 10% tax on Canadian oil imports will slam refineries in the Midwest that were built to take Canada’s crude oil, which is cheaper and heavier than most U.S. crude, and are expensive to adapt, especially if the tariffs are only a passing fancy. “You can’t turn the Titanic on a dime, and the industry is kind of the same way,” Rick Weyen, a retired refining executive, told the New York Times.

- Ford is angry: U.S. executives have been largely silent so far on Trump’s economic plans, but not Ford Motor CEO Jim Farley. He says Ford may have to lay off workers if Trump goes ahead with tariffs on Mexico and Canada, and cuts tax breaks for EVs. If Republicans repeal Biden-era legislation that provided billions in EV factory loans and subsidies, “many of those jobs will be at risk,” Farley told an investment conference. “A 25 percent tariff across the Mexico and Canadian border will blow a hole in the U.S. industry that we have never seen,” he added. “It gives free rein to South Korean and Japanese and European companies that are bringing one and a half to two million vehicles into the U.S. that wouldn’t be subject to those Mexican and Canadian tariffs.” Trump’s plans have not been helpful, Farley said. “So far what we’re seeing is a lot of costs and a lot of chaos.”

Attention Walmart Shareholders!

Shares in America’s biggest retailer dropped more than 6% by midday Thursday after the company said its 2026 fiscal-year revenue and profit targets would be below Wall Street analysts’ expectations. Investors had been piling into the stock as budget-conscious consumers flocked to its stores and website. This boosted revenue and profits, pushing shares up more than 66% in the past 12 months. However, continued consumer wariness, stubborn inflation, and the threat of tariffs on imported foods (plus the threat of rising labor costs or shortages on domestic producers) have cut hopes that growth will continue at the same pace. “Wallets are still stretched,” John David Rainey, Walmart’s chief financial officer, told The Wall Street Journal. About two-thirds of what Walmart sells is made, grown, or assembled in the U.S., but if tariffs on goods from Mexico and Canada take effect, Rainey told CNBC, Walmart is “not going to be completely immune.”

Peter S. Green is a veteran reporter and editor who has spent more than two decades covering business and finance from Eastern Europe to New York City, and has worked for Bloomberg News, The New York Post, The New York Times and The Messenger. He lives in New York City and is always looking for the next big story.