An empty restaurant serving only takeout due to the novel coronavirus, COVID-19, outbreak is seen in Washington, DC, on March 18, 2020. (Photo by NICHOLAS KAMM / AFP) (Photo by NICHOLAS KAMM/AFP via Getty Images)

JPMorgan Chase will invest $8 million in small businesses in the U.S., Europe, and China that have been hit hard by the public health and economic impacts of the COVID-19 crisis.

The investment is part of a much larger $50 million global philanthropic commitment to help provide emergency healthcare, food, and other humanitarian relief to vulnerable communities and existing nonprofit partners.

Chase will deploy the first $15 million “promptly” and the remainder over time. As consumers self-quarantine and cities go on lockdown, small businesses have already been majorly disrupted by the pandemic and are preparing for much worse over the coming weeks.

About half of small businesses have 14 or fewer cash buffer days, according to a JPMorgan research report on small business financial health in urban communities. In black or Hispanic communities, most small businesses have fewer than 21 cash buffer days.

Chase is working with its customers, including small businesses, to waive fees, extend payment due dates for cards, auto loans, and mortgages, and increase credit lines as needed due to coronavirus-related challenges, a spokesman for the company said.

Like most banks, it’s also directing people to its mobile app, but many small businesses still require branches to make change for drawers and to deposit cash.

The bank’s financial commitment follows one by Facebook, which said Tuesday it would invest a whopping $100 million in now struggling small businesses. Delivery startups like Grubhub and DoorDash are deferring or waiving commissions to encourage people to continue giving business to independent local restaurants.

Candace Mitchell Harris discusses her path from computer scientist to founder of beauty tech tool MYAVANA – and how it uses A.I. to analyze each person’s unique haircare needs.

Michael Harris, NYSE global head of capital markets shares what to expect from IPOs in 2024, including A.I. excitement and why interest rate cuts are always helpful.

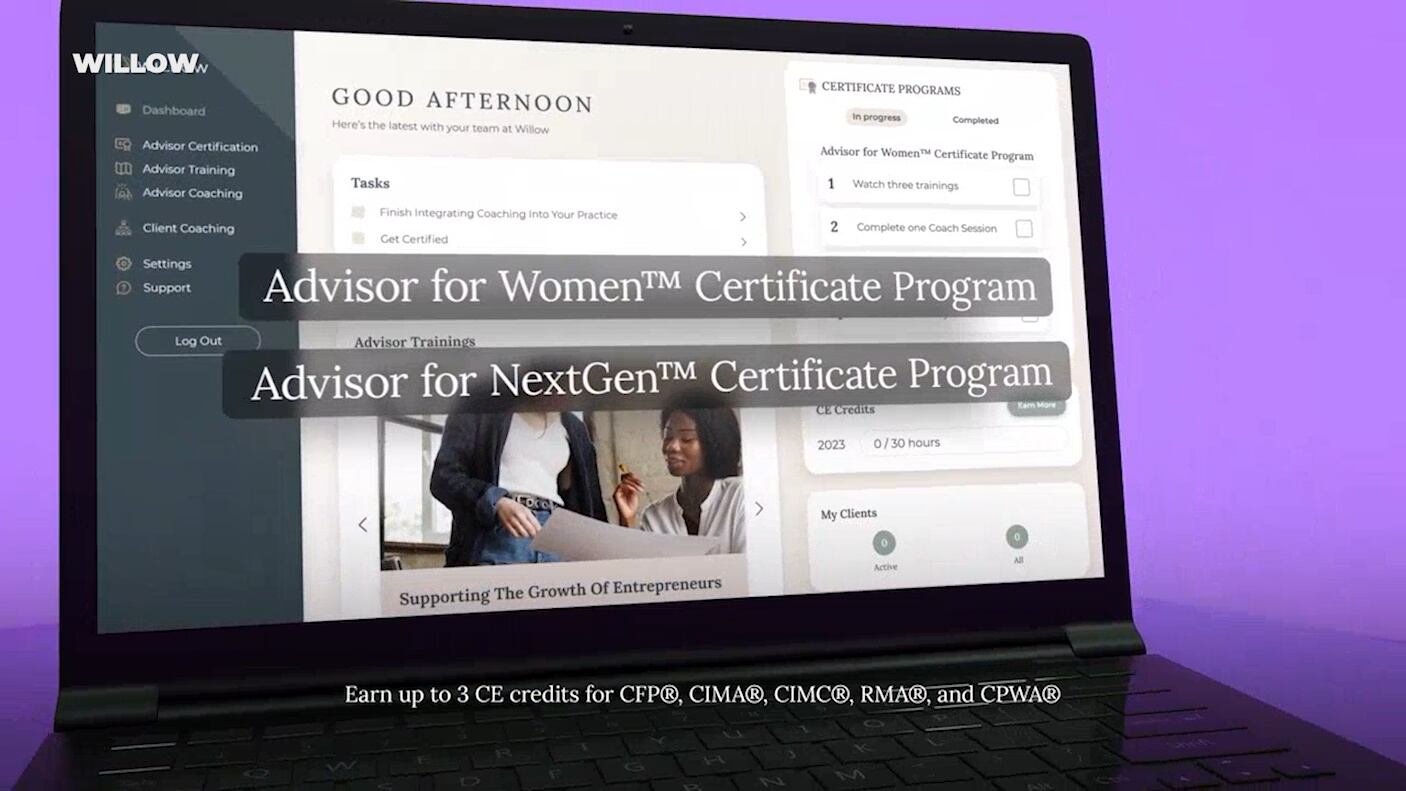

Lacy Garcia, Founder & CEO of Willow, shares why women, traditionally underserved by fintech, are looking for trust and a personal relationship from their financial advisor.

Alexander Reed, CFA and CIO for Envisage Wealth, breaks down why he thinks rates could stay higher for longer and why real estate, utilities, and regional banks are sectors to avoid.

Big brands that have relied on TikTok videos to reach younger consumers do not appear to be panicking as they wait to see what happens. But they have started planning.

It's been 15 years since the last fatal crash of a U.S. airliner, but you wouldn't know that from a torrent of flight problems that made news in the last three months.

Abortion opponents want the high court to ratify a ruling from a conservative federal appeals court that would limit access to a medication called mifepristone, which was used in nearly two-thirds of abortions last year.

Annie Chechitelli, chief product officer at Turnitin, breaks down how students and teachers alike can learn from artificial intelligence – while still maintaining academic integrity.